The Role of Computerized Accounting Applications as one of the Requirements of the Labor Market in Accounting Education Curricula

DOI:

https://doi.org/10.21271/zjhs.30.2.3Keywords:

Computerized accounting applications, labor market requirements, accounting education curricula.Abstract

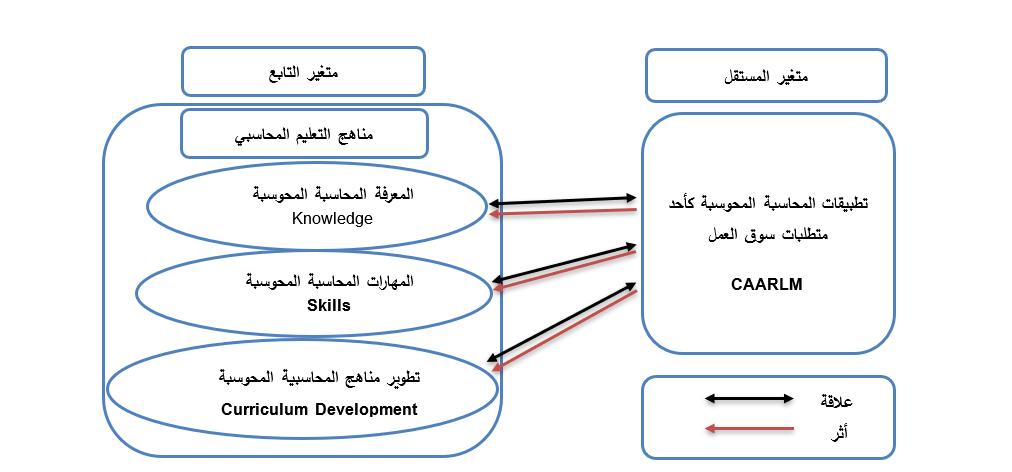

This research aims to reveal the extent of the existing gap between the requirements of the labor market in the Kurdistan Region, in light of the increasing reliance on computerized accounting, and the accounting education curricula through (computerized accounting knowledge, computerized accounting skills, and accounting curriculum development), with the aim of providing a scientific basis to rely on when planning for future curriculum development. To achieve the objectives of the study and verify its hypotheses, a questionnaire consisting of two parts was prepared. The first part includes paragraphs aimed at identifying the characteristics of the research sample, and the second part includes (60) paragraphs that were used in collecting data with the aim of testing the hypotheses and answering questions related to the research problem. It was distributed to a sample of company owners and managers in Duhok Governorate and Zakho Independent Administration. The research sample numbered (72) individuals.

The results of the statistical analysis revealed a significant positive correlation between the use of computerized accounting applications as a labor market requirement and accounting education curricula. This correlation spans three main axes: knowledge of computerized accounting, related skills, and curriculum development aligned with these applications. These results highlight the importance of computerized accounting applications as essential tools for developing the capabilities of accounting graduates, both in terms of theoretical knowledge and practical skills. Accordingly, the study recommends updating accounting education curricula to align with the latest digital accounting programs and applications used in the contemporary business environment. It also emphasizes the importance of enhancing cooperation between accounting departments, sector committees, and curriculum development directorates at the region's universities to ensure the development of educational content that aligns with labor market needs and bridges the gap between education and practice.

References

6.المصادر باللغة العربية

- أحمد محمد شوقي محمد فهي. (2023). نضج الصناعة في تطبيق المحاسبة السحابية كمتغير معدل للعلاقة بين معلومات المحاسبة السحابية وقرار الاستثمار في أنظمتها. مجلة البحوث المحاسبية. (4). 769-845.

- جعفر حسن جاسم الطائي. (2022). جودة مخرجات التعليم العالي ودورها في سد احتياجات سوق العمل نحو تـــــنمية مســــتدامة في التعـــليم الـــعــــالـــي والبحث العلمي. مجلة ديالى للبحوث الإنسانية. (95).3. 308-332.

- حسان، & محمد صبحي جمعة. (2018). مدى توافق التعليم المحاسبي مع متطلبات سوق العمل (دراسة ميدانية). على المؤسسات والجمعيات الأهلية المحلية في قطاع غزة. رسالة ماجستير.

- درويش، & عمار. (2017). متطلبات تحسين جودة التعليم المحاسبي في الجزائر (دراسة قياسية). مجلة المالية والأسواق. (4).1. 270-292.

- رحب محمد عبد الحسيب، & محمد بکري موسي، (2017). تصور مقترح للاستفادة من خدمات الحوسبة السحابية بالجامعات المصرية في ضوء التوجه نحو مجتمع المعرفة الرقمي. مجلة کلية التربية. بنها,28(2) , 211-262.

- سوران محمد أمين حبيب. (2023). مدى إدراك مراقبي الحسابات في التعامل مع البرامج المحاسبية المحوسبة وأثره على مخاطر التدقيق وانعكاسه على جودة التدقيق. أطروحة دكتوراه غير منشورة. كلية التقنية الإدارية. جامعة السليمانية التقنية. العراق.

- علي علي العنسي. (2022). مدى إيفاء التعليم المحاسبي بمتطلبات سوق العمل دراسة ميدانية في السوق السعودي. مجلة جامعة الأنبار للعلوم الاقتصادية والإدارية. (14).3. 524-540.

- الفكي، & الفاتح الأمين. (2014). تصور مقترح لتطبيق معايير التعليم المحاسبي ودورها في ضبط مناج المحاسبة في الجامعات السعودية. (دراسة الوصفية). المجلة العربية لضمان الجودة. (7).16. 109-138.

- هجيره بوعزرية، & نبيلة لندار. (2017). واقع التعليم المحاسبي في الجامعات الجزائرية في ظل التوجه نحو تطبيق معايير الإبلاغ المالي الدولية (IFRS)-دراسة استبيانيه في جامعة الجيلالي بونعامة.

- وسام عزيز شناوة، & حسين كريم الشمري. (2019). المحاسبة السحابية أفق جديد لتنظيم العمل المحاسبي. مجلة كلية مدينة العلم الجامعة. (11).1.

6.المصادر باللغة الأجنبية

- Akande O. O. (2016). Computerized accounting system effect on performance of enterprises in South Western Nigeria. Proceedings of ISER International Conference, Birmingham, (1).2.11-28.

- Althebeh, Z. A. (2019). Impact of accounting information system on reducing liquidity risk in Saudi banks comparative study between Islamic banks and commercial banks. Academy of Accounting and Financial Studies Journal, 23(1), 1-11.

- Howieson, B. (2003). Accounting practice in the new millennium: is accounting education ready to meet the challenge? The British Accounting Review, 35(2), 69-103.

- Ismael, B. A., Ahmed, R. A., Yaba, J. A., Hamawandy, N. M., Abdullah, R., Jamil, D. A., & Sulaiman, A. A. (2020). The Effects of Computerized Accounting System on Auditing Process: A Case Study from Northern Iraq. Jain 2020.

- Martha, G. I. R., & Subriadi, A. P. (2019, May). A Literature Review− Firm Investment on Cloud as Efficient & Effective Technology. In Journal of Physics: Conference Series (Vol. 1201, No. 1, p. 12007). IOP Publishing.

- Quang, L. H. (2019). The relationship between organizational performance and computerized accounting: The role of business environment. International Journal of Humanities and Social Science Invention (IJHSSI), 6(8), 62-68.

- Rashid, C. A., & Jaf, R. A. S., (2023), The Usefulness of The Capital Asset Pricing Model in Predicting Total Shareholder Return. Zanco Journal of Humanity Sciences, 27(1), 408-416.

- Saber, Rizgar A Saber, Al-Shatnawi, Hassan M Al-Shatnawi, Muhammad, Nakhshin J Muhammad (2023), (Reflection of the Advantages of Using Digital Transformation Technologies on Achieving Competitive Price), Polytechnic Journal of Humanities and Social Sciences,4 (2) 881-891.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Honar Haji Hasan , Farhad Hasan Sulaiman, Rizqar Abdullah Sabir

This work is licensed under a Creative Commons Attribution 4.0 International License.