The Impact of Activity Based Costing (ABC) on Cost Reduction

DOI:

https://doi.org/10.21271/zjhs.28.6.17الكلمات المفتاحية:

التكلفة على أساس النشاط، تخفيض التكلفة، السعر التنافسي.الملخص

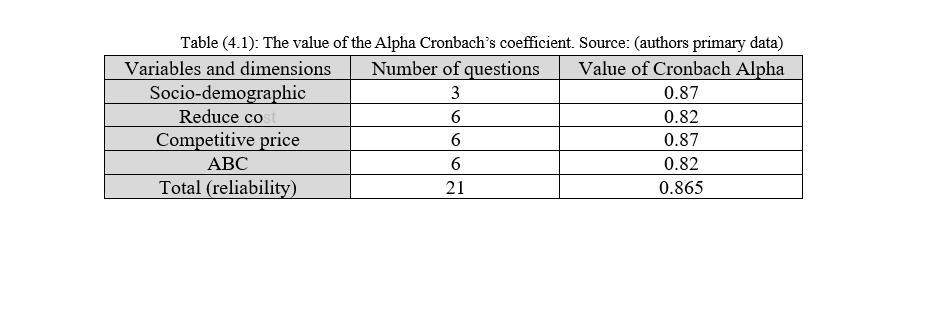

This study examines the impact of Activity-Based costing technique (ABC) on cost reduction and competitive price in the number of industrial firms in Erbil city in the Kurdistan Region- Iraq. The objective of the study investigates the impact of activity-based costing technique on cost reduction and competitive price. This study used quantitative method for determine and describe results and a survey questionnaire for collecting data on manufacturing firms in Erbil city, Kurdistan region of Iraq. Also. Randomly distributed 125 questionnaire forms on specific employees and collecting 87 forms. This research study used the Statistical Package for the Social Sciences (SPSS 26) software program to analyze collected data. The study also tested the correlation and simple regression models. The results provided a significant relationships and impact exist between activity-based costing technique with cost reduction and significant relationship and significant impact with competitive price. The model was approved to give a clear reliability test by applying alpha Cronbach test. Moreover, the study model constructs to explain the concern relationship between activity-based costing technique and product value.

المراجع

- Abu Nassar, M. (2017), Cost Accounting, Dar Wael, Amman, Jordan.

- Babaaddoun Messaoud & Ait-Mohammed Mourad, (2021). The comparison between Activity Based Costing and Traditional Costing that practiced in Algerian Manufacturing Corporation, International journal of economic performance Volume:04 Issue:03 Year:2021.

- Bruce A, M, (1992). Aspects of cost control. Cost Engineering, 34(6), 19.

- Cooper, R. G. (1994). New products: the factors that drive success. International marketing review, 11(1), 60-76.

- Cooper, R., and Kaplan, R.S., (1988). Measure costs right: make the right decisions. Harvard business review, 66(5), 96-103.

- Cooper, R., Kaplan, R.S. (1991). Profit priorities from activity-based costing. Harvard business review, 69(3), 130-135.

- Eman Ahmad Al Hanini, (2018). The impact of adopting Activity Based Costing (ABC) on decreasing cost and maximizing profitability in industrial companies listed in Amman Stock Exchange. Academy of Accounting and Financial Studies Journal, 22(5), 1-8.

- Fatah, R. D., & Jaf, R. A. S. (2023). Green Concepts And Material Flow Cost Accounting Applications For Manufacturing Company: Approach For Company Sustainability. Russian Law Journal, 11(9s).

- Hamad, Qabil Zrar; Sabir, Rzgar Abdulla,(2023).The Impact Of Concurrent Engineering (Ce) Technique On Improve Value Of Product. Webology . Vol. 20 Issue 3, P33-58. 26p.

- Hamad. Qabil Zrar. (2015). the relationship between monetary policy instruments and Turkish stock market (Master thesis) near east university.

- Horngren, T.C., Foster, G. and Datar, M.S. (2010). Cost accounting: a managerial emphasis. Issues in accounting education, 25(4), 789-790.

- Jaf ,Rizgar Abdullah Sabir(2015) .The Role of Mark to Market on the Properties of Accounting Information in Kurdistan International Bank . Research Journal of Finance and Accounting www.iiste.org ISSN 2222-1697 (Paper) ISSN 2222-2847 (Online) Vol.6, No.4.

- Jaf, R. S & Xinping, X.(2011). Possibility Realized Competitive Advantage By Strategic Information Systems Evidence From Iraqi Banks. Annual Summit on Business and Entrepreneurial Studies. Pp.247-265.

- Kaplan, R. S., & Cooper, R. (1988). Cost and effect: Using integrated cost systems to drive profitability and performance. Boston: Harvard Business School Press.

- Khzer,Karzan Adnan & Jaf, Rizgar Abdullah Sabir(2023),The Role Of Income Smoothing On Financial Performance Indicators. 3c Empresa: Investigación Y Pensamiento Crítico, Issn-E 2254-3376, Vol. 12, Nº. 2, 2023, Págs. 362-376.

- Kluemper, D.H., Little, L.M. and De Groot, T. (2009) State or Trait: Effects of State Optimism on Job-Related Outcomes. Journal of Organizational Behavior. https://doi.org/10.1002/job.591.

- Lai, A.W. (1995). Consumer values, product benefits and customer value: A consumption behavior approach. Advances in Consumer Research, 22, eds. Frank R. Kardes and Mita Sujan, Provo, UT: Advances for Consumer Research.

- Lee, K., Carter, S. (2005). Global marketing management. Strategic Direction, 27(1).

- Leezenberg, Michiel. “polıtıcs, economy, and ıdeology ın Iraqı Kurdistan sınce 2003: endurıng trends and novel challenges.” The Arab Studies Journal 23, no.1 (2015). http://www.jstor.org/stable/44744903.

- Lewis, R. J. (2015). Activity-based models for cost management systems. Quorum Books, Westport, CT.

- Mustafa, A. M., Azimli, A., & Sabir Jaf, R. A. (2022). The Role of Resource Consumption Accounting in Achieving Competitive Prices and Sustainable Profitability. Energies, 15(11), 4155.

- Masadeh, A. (2023). Application of Using the Activity-Based Costing System on Product Development in Jordan’s Manufacturing Listed Manufacturing Firms. International Journal of Professional Business Review, 8(6), e02458-e02458.

- McCormick, T, (2010), Strategic Cost Reduction Steps to Success, Accountancy Ireland.

- Muhajir, H, S. (2015). Academic performance of undergraduate students at Soran University in Northern Iraq. IJARET, 2(4), 92-7.

- Nair, S., & Tan, X. (2018). Factors influencing the implementation of activity–based costing: a study on Malaysian SMEs. International Business Research, 11(8), 133-141.

- Nitin Kumar & Dalgobind Mahto, (2013), Current trends of application of activity-based costing (ABC): A review. Global Journal of Management and Business Research Accounting and Auditing, 13(3).

- Osisioma, B. C & Enahoro. C. (2006). Activity Based Costing: Journal of Global Accounting. Department of Accounting Nnamdi Azikiwe University.

- Rao, A. & Monroe, K. (1988). The moderating effect of prior knowledge on cue utilization in product evaluations. Journal of consumer research, 15(2), 253-264.

- Sabir, R. A., & Mahmood, S. (2023). The Impact of Sustainable Balance Scorecard to Achieve Competitive Advantage in the Kurdistan Region of Iraq Economic Unit. Journal of University of Raparin, 10(3), 750–781. https://doi.org/10.26750/Vol(10).No(3).Paper33

- Sabir Jaf, A., (2020). The Role of Open Book Costs Accounting (OBCA) in Supporting Competitive Advantage. International Journal of Advanced Science and Technology, 29(2), pp. 3103-3113.

- Sheth, J. N., Newman, B. I. and Gross, B. L. (1991). Why we buy what we buy: A theory of consumption values. Journal of business research, 22(2), 159-170.

- Tanju, D.W., Helmi, M. (1991). ABCs for internal auditors. Internal Auditor, 48(6), 33-38.

- Theeuwes and Andriaanson, (2014). Towards an integrated accounting framework for manufacturing improvement. International Journal of Production Economics, 36(1), 85-96.

التنزيلات

منشور

كيفية الاقتباس

إصدار

القسم

الرخصة

الحقوق الفكرية (c) 2024 Qabil Zrar Hamad, Khalis Mheadin Qadir, Muhamad Khoshawi Mustafa, Muhamad Azad Azeez, Shifa Arif Omer

هذا العمل مرخص بموجب Creative Commons Attribution 4.0 International License.