The Effectiveness of Implementation Material Flow Cost Accounting (MFCA): A Case Study in The Standard Concrete Company in Duhok

DOI:

https://doi.org/10.21271/zjhs.30.3.12Keywords:

EMA, MFCA, Cost Reduction Waste-Free Production Competitive priceAbstract

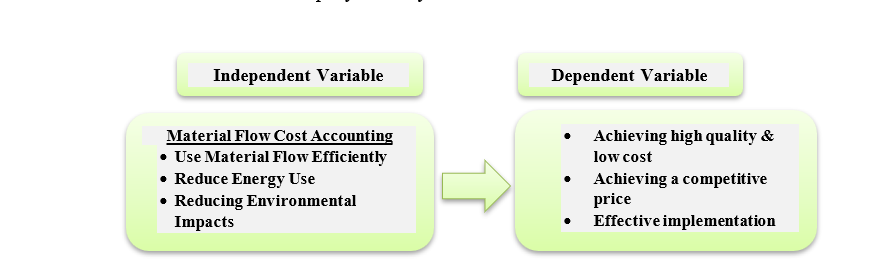

This study aims to explore the role of Material Flow Cost Accounting (MFCA) in enhancing both financial and environmental performance in industrial companies. The importance of this research stems from the fact that MFCA is one of the most advanced techniques in environmental management accounting, providing quantitative and monetary data that contribute to improving cost control and supporting decision-making processes, thereby achieving competitive pricing advantages. The study adopted a descriptive–analytical approach by analyzing data and reports of Standard Concrete Company in Duhok during the study period. It tested the research hypotheses, highlighted the main challenges facing MFCA implementation, and demonstrated the limitations of traditional costing systems. The findings revealed that the application of MFCA effectively reduces costs and supports competitive pricing policies, as it provides accurate data on emissions, waste, and costs related to both positive and negative products. The analysis showed that positive outputs accounted for 96.126%, while negative outputs represented 3.874%, which included 77,745 liters of water, 5,874 electricity units, 4,226 liters of fuel and lubricants, 261 tons of cement, 460 tons of sand, 280 tons of gravel, and 453 cubic meters of concrete debris. The study concluded that MFCA can be successfully implemented in Standard Concrete Company and plays a pivotal role in reducing waste, cutting costs, and promoting cleaner production. It recommends expanding the application of MFCA in other industrial firms and emphasizes the importance of forming specialized and well-trained teams in modern cost and management accounting practices to address environmental and technological challenges.

References

- Ahmed, N., Ali, M. A. and Sana, M. (2024) ‘Application of material flow cost accounting (MFCA) in waste reduction: A case study on small and medium-scaled enterprise (SME) corrugation packages industry’, Journal of Material Cycles and Waste Management, 26, pp. 3217–3247. https://doi.org/10.1007/s10163-024-02039-w

- Christ, K. L. and Burritt, R. L. (2016) ‘ISO 14051: A new era for MFCA implementation and research’, Revista de Contabilidad–Spanish Accounting Review, 19(1), pp. 1–9.

- Dekamin, M. and Barmaki, M. (2019) ‘Implementation of material flow cost accounting (MFCA) in soybean production’, Journal of Cleaner Production, 210, pp. 459–465. https://doi.org/10.1016/j.jclepro.2018.11.057

- Doorasamy, M. (2015) ‘Theoretical developments in environmental management accounting and the role and importance of MFCA’, Foundations of Management, 7(1), pp. 37–52.

- Doorasamy, M. (2019). Material flow cost accounting practices and resource efficiencies in South African sugar industry. Doctoral dissertation.

- Elgably, W. S. A. and Abou Nel, S. A. M. (2023) ‘A proposed framework for the integration between Material Flow Cost Accounting (MFCA) and the Target Costing method (TC) to reduce costs and support the competitive advantage of business enterprises: A field study’, Alexandria Journal of Accounting Research, 7(1), pp. 353–430. https://doi.org/10.21608/aljalexu.2023.288772

- Fakoya, M. B. (2014) ‘An adjusted material flow cost accounting framework for process waste-reduction decisions in the South African brewery industry’, Doctoral dissertation, University of South Africa.

- Fatah, R. D. and Jaf, R. A. S. (2023) ‘Green concepts and material flow cost accounting applications for manufacturing company: Approach for company sustainability’, Russian Law Journal, 11(9s).

- Horngren, C., Foster, G. and Datar, S. (2017) Cost Accounting: A Managerial Emphasis. 16th edn.

- Hyršlová, J., Vágner, M. and Palásek, J. (2011) ‘Material flow cost accounting (MFCA) – tool for the optimization of corporate production processes’, Business, Management and Economics Engineering, 9(1), pp. 5–18.

- Jasch, C. (2009) ‘What is EMA and why is it relevant? Environmental and Material Flow Cost Accounting: Principles and Procedures’, pp. 1–35.

- Kovanicová, D. (2011) ‘Material flow cost accounting in Czech environment’, European Financial and Accounting Journal, 6(1), pp. 7–18.

- Mohsin, A. A. and Mohammed, H. H. (2025) ‘Importance of implementing material flow cost accounting technique (MFCA) and its role to enhance environmental sustainability in industrial companies: An analytical study on a set of refining companies / Erbil’, Journal of Accounting and Financial Studies, 20(71).

- Mustafa, A. M., Azimli, A. and Jaf, R. A. S. (2022) ‘The role of resource consumption accounting in achieving competitive prices and sustainable profitability’, Energies, 15(11), 4155. https://doi.org/10.3390/en15114155

- Rashid, C. A. and Jaf, R. A. S. (2023) ‘The usefulness of the Capital Asset Pricing Model in predicting total shareholder return’, Zanco Journal of Humanity Sciences, 27(1), pp. 408–416.

- Sahu, A. K., Padhy, R. K., Das, D. and Gautam, A. (2021) ‘Improving financial and environmental performance through MFCA: A SME case study’, Journal of Cleaner Production, 279, 123751. https://doi.org/10.1016/j.jclepro.2020.123751

- Saunders, E. N. (2009) ‘Transformative choices: Leaders and the origins of intervention strategy’, International Security, 34(2), pp. 119–161.

- Tajelawi, O. A. and Garbharran, H. L. (2015) ‘MFCA: An environmental management accounting technique for optimal resource efficiency in production processes’, World Academy of Science, Engineering and Technology.

- Tran, T. T. and Herzig, C. (2020) ‘Material flow cost accounting in developing countries: A systematic review’, Sustainability, 12(13), 5413. https://doi.org/10.3390/su12135413

- Walls, C., Putri, A. R. K. and Beck, G. (2023) ‘Material flow cost accounting as a resource-saving tool for emerging recycling technologies’, Clean Technologies, 5(2), pp. 652–674. https://doi.org/10.3390/cleantechnol5020033

- Yagi, M. and Kokubu, K. (2018) ‘Corporate material flow management in Thailand: The way to material flow cost accounting’, Journal of Cleaner Production, 198, pp. 763–775.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Salam Rasheed Fathi AL-Mizori , Rizgar Abdullah Jaf, Anas Fatah Omar

This work is licensed under a Creative Commons Attribution 4.0 International License.