The Impact of Applying International Accounting and Financial Reporting Standards (Ifrss/Iass) on the Financial Performance of Iraqi Banks: an Applied Study on a Sample of Banks Listed on the Iraqi Stock Exchange

DOI:

https://doi.org/10.21271/zjhs.29.SpC.34Keywords:

Accounting and financial reporting standards, Iraq Stock Exchange, financial analysis indicatorsAbstract

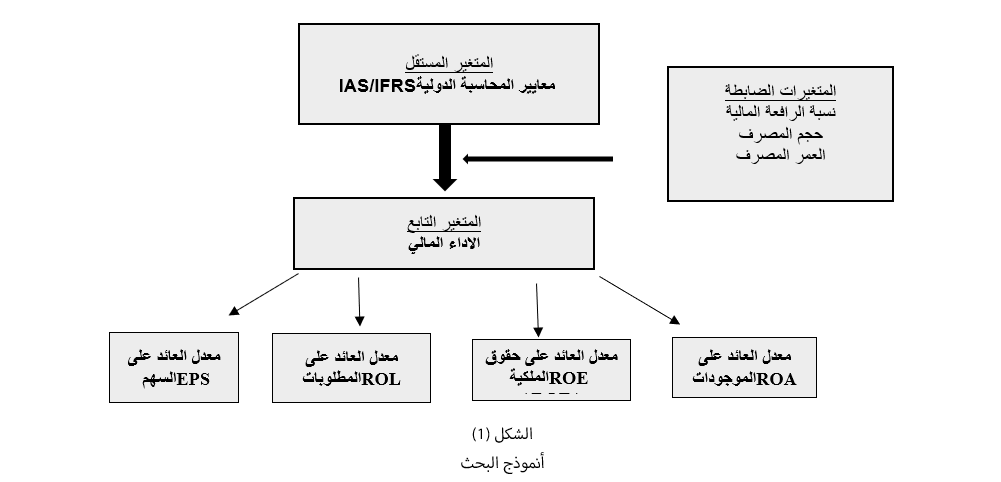

The study aimed to determine the impact of implementing International Accounting and Financial Reporting Standards (IAFS) on the financial performance of Iraqi banks listed on the Iraq Stock Exchange for the period 2012-2021. To achieve this, the researchers analyzed the annual financial reports of twelve Iraqi joint-stock banks listed on the market and extracted the following study variables: return on assets, return on equity, return on liabilities, return on equity, implementation of IAFS, bank size, bank age, and leverage ratio. The study employed content analysis of the financial reports of Iraqi banks. The results showed that the four multiple regression models used were highly statistically significant, allowing for reliable prediction of the values of the dependent variables. The results also showed that the estimated variance inflation coefficient values for all independent variables were less than 5, indicating the absence of multicollinearity. The results also revealed a statistically significant negative relationship between the implementation of IAFS and the financial performance of Iraqi banks across variables and during the period. The study presented several recommendations, including the need for banks registered on the Iraq Stock Exchange to standardize the procedures and rules used in preparing financial statements, which would facilitate comparisons between banks' financial performance. Accounting researchers should also focus on research and studies that address international financial reporting standards and their impact, taking into account other variables, particularly the Iraqi business environment.

References

بشناق، زاهر صبحي(2011)، تقييم الاداء المالي للبنوك الاسلامية والتقليدية باستخدام المؤشرات المالية (دراسة مقارنة للبنوك الوطنية العاملة في فلسطين)، رسالة ماجستير، كلية التجارة، الجامعة الاسلامية ، غزة.

جواد، انتصار محمد (2012)، تقييم الاداء المالي للمصارف العراقية في ضوء معايير لجنة بازل دراسة تحليلية في مصرف الرشيد، مجلة الكوت للعلوم الاقتصادية والادارية، (8)، 172-197.

الصفار، نور عبد السالم خليل (2022)، تأثير تطبيق معايير اإلبالغ المالي الدولية IFRSs على مخرجات النظام المحاسبي الموحد في العراق بالتطبيق على الشركة العامة للسمنت الشمالية، رسالة ماجستير غير منشورة، جامعة موصل.

عثمان، فاضل نبي و مخلص، جنار اسماعيل(2022)، مدى إمكانية التزام الشركات بتطبيق معيار التقرير المالي الدولي 15 IFRS "الإيرادات الناتجة من العقود مع العملاء" و انعكاسه على قرارات مستخدمي القوائم المالية : دراسة استطلاعية تحليلية لآراء عينة من الموظفين المعنيين في الشركات إقليم كوردستان-العراق (محافظة أربيل أنموذجا)، مجلة زانكو للعلوم الإنسانية، المجلد 26، العدد 1 1-26. https://doi.org/10.21271/zjhs.26.1

المخموري، عدنان نادر حمد(2019)، العوامل المؤثرة في توقيت اصدار التقارير المالية السنويةدراسة تطبيقية عل عينة من المصاف العراقية المدرجة في سوق العراق اللاوراق المالية، مجلة زانكو للعلوم الإنسانية، المجلد 23، العدد 4 ، 11-34. 10.21271/zjhs.23.4.2

الفار، سماح عفيف عاشور (2018): العوامل المؤثرة على الأداء المالي للشركات غير المالية المدرجة في بورصة فلسطين باستخدام نموذج (Tobin's q)، رسالة ماجستير، جامعة الأزهر- غزة، فلسطين.

الموسوي، انعام محسن غدير(2015)، تشخيص محددات ومزايا التحول إلى معايير التقارير المالية الدولية (IFRS (من منظور مستخدمي المعلومات :دراسة تحليلية للمصارف الأهلية العاملة في محافظة النجف الاشرف،مجلة الغري ،للعلوم الاقتصادية والادارية،المجلد13 ،العدد 36.

الشجيري، محمد حويش علاوي، (2020)، المحاسبة الدولية ومعايير الابلاغ المالي، الطبعة الاولى، الجامعة العراقية، بغداد، العراق.

ثانيا: المصادر باللغة الاجنبية:

Aksoy, Emine Ebru and Yildiz Ayse (2017) Applying Data Envelopment Analysis to Evaluate Firm Performance, Global Business Strategies in Crisis, p319-334. DOI: 10.1007/978-3-319-44591-5_22

Burca, V., & Almasi, R. (2019). Analysis of the Impact of Changes to International Financial Reporting Standards, on the National Accounts Dashboard. Acta Universitatis Danubius. Economica, 15(6), 115-135

Hinggins Robert C. “Analysis for Financial Management" 10th ed, McGraw-Hill 2012.

Hoshino. (2017). Effect of IFRS Adoption on Corporate Performance Meas- urement: Analysis of Japanese Manufacturing Companies. Journal of Accounting and Finance, 5(4), 78-90.

Houqe, M., Monem, R. & Zijl, T., (2016), the economic Consequences of IFRS adoption: Evidence from New Zealand, Journal of international Accounting, Auditing and Taxation, Vol. 27, p.p.40-48.

Kamath, R., & Desai, R. (2014). The Impact of IFRS Adoption on the Financial Activities of Companies in India: An Empirical Study. IUP Journal of Accounting Research & Audit Practices, 13(3), 25-36. 32/38

Krishnan, G. V., & Zhang, J. (2019). Does mandatory adoption of IFRS enhance earnings quality? Evidence from closer to home. The International Journal of Accounting, 54(01),

Wibowo, D., (2022),”Analysis of the Effect of Islamic Corporate Governance on the Financial Performance of Islamic Banking in Indonesia”, Jurnal Ilmiah Ekonomi Islam, Vol 8, No 3. 3501-3506, dx.doi.org/10.29040/jiei.v8i3.6799

Yundi, NF, & Sudarsono, H. (2018). The effect of financial performance onthe return on assets (ROA) of Islamic banks in Indonesia. Al-Amwal: Journal of Sharia Economics and Banking, 10 (1), 18-31.

Purwanto, Purwanto & Isnain Bustaram, & Subhan, Zef Risal, (2020),The Effect of Good Corporate Governance on Financial Performance in Conventional and Islamic Banks: An Empirical Studies in Indonesia, International Journal of Economics and Financial Issues 10(3):1-6

المواقع الالكترونية:

- هيئة الاوراق المالية العراقية (www.isc.gov.iq)

- سوق العراق للاوراق المالية (www.isx-iq.net).

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Adnan Nader Hammed Makhmury, Sanaa Jamel Maulood

This work is licensed under a Creative Commons Attribution 4.0 International License.